Featured

Table of Contents

Examples of other loans that aren't amortized include interest-only loans and balloon loans. The previous includes an interest-only period of payment, and the latter has a large primary payment at loan maturity. An amortization schedule (often called an amortization table) is a table detailing each periodic payment on an amortizing loan.

Each repayment for an amortized loan will include both an interest payment and payment towards the primary balance, which differs for each pay period. An amortization schedule helps indicate the specific quantity that will be paid towards each, along with the interest and principal paid to date, and the remaining primary balance after each pay duration.

Normally, amortization schedules just work for fixed-rate loans and not adjustable-rate home loans, variable rate loans, or lines of credit. Certain businesses in some cases acquire costly products that are utilized for long durations of time that are categorized as investments.

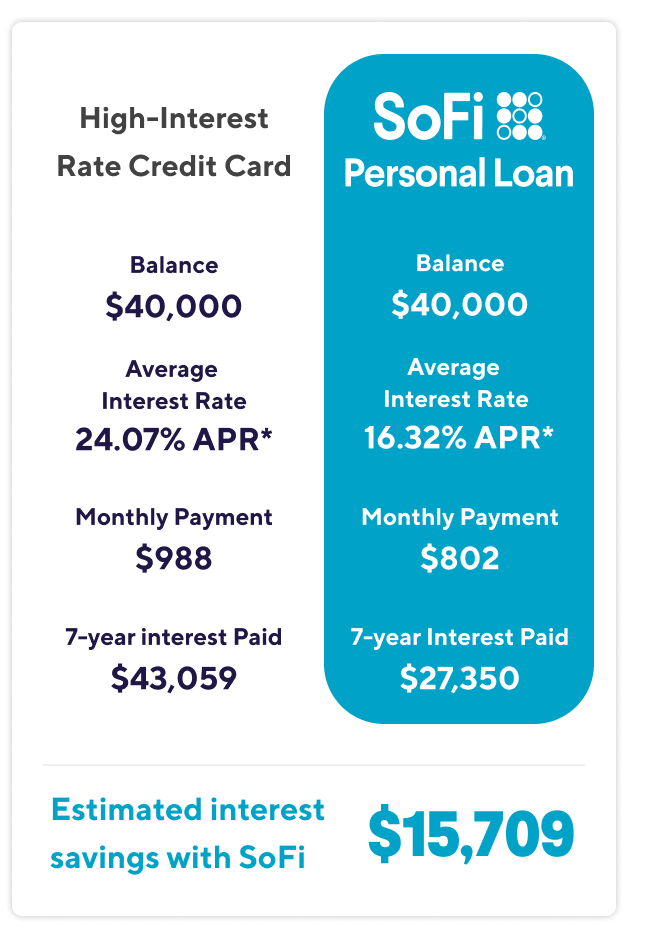

Best Ways to Reduce Credit Balances

Although it can technically be thought about amortizing, this is generally described as the depreciation expense of an asset amortized over its expected life time. For more information about or to do estimations including depreciation, please visit the Depreciation Calculator. Amortization as a way of spreading business expenses in accounting usually describes intangible properties like a patent or copyright.

law, the value of these assets can be deducted month-to-month or year-to-year. Simply like with any other amortization, payment schedules can be anticipated by a determined amortization schedule. The following are intangible possessions that are typically amortized: Goodwill, which is the reputation of an organization considered as a quantifiable asset Going-concern value, which is the worth of a service as an ongoing entity The workforce in location (current employees, including their experience, education, and training) Service books and records, running systems, or any other details base, including lists or other info worrying current or prospective clients Patents, copyrights, formulas, procedures, designs, patterns, knowledge, formats, or comparable items Customer-based intangibles, including customer bases and relationships with clients Supplier-based intangibles, consisting of the worth of future purchases due to existing relationships with suppliers Licenses, allows, or other rights given by governmental systems or companies (consisting of issuances and renewals) Covenants not to contend or non-compete arrangements entered connecting to acquisitions of interests in trades or organizations Franchises, trademarks, or trade names Contracts for making use of or term interests in any products on this list Some intangible properties, with goodwill being the most typical example, that have indefinite useful lives or are "self-created" may not be lawfully amortized for tax functions.

Understanding Repaired and Variable Combination AlternativesIn the U.S., company startup costs, defined as expenses incurred to investigate the capacity of creating or obtaining an active service and costs to produce an active business, can only be amortized under specific conditions. They should be costs that are deducted as overhead if sustained by an existing active service and should be incurred before the active company begins.

According to IRS standards, preliminary start-up expenses must be amortized.

Toggle navigation Loan 1 Loan 2 $1,060.66 $988.86 $127,278.44 $118,662.99 $27,278.44 $18,662.99 Mar 2036 Mar 2036

Comparing Multiple Debt Payoff Strategies for 2026

This Loan Payment Calculator computes a quote of the size of your regular monthly loan payments and the annual salary required to manage them without excessive financial problem. The calculator can be utilized with Federal education loans (Direct Subsidized, Unsubsidized, and PLUS) and most private trainee loans. You can also utilize the loan calculator to calculate auto loans or home mortgage payments.

Different parts can affect your loan payments, consisting of credit ratings, the schedule of a co-signer, the loan amount, loan benefit dates, lender requirements, and more. Below are a few of the most common factors that will impact your loan payment: The loan includes the general amount required for a semester or year.

Other elements, such as charges and loan rates of interest, will make the quantity paid greater than the initially asked for loan overall. A rates of interest is the portion of a borrower's loan amount paid back in addition to the initial loan quantity. The greater the interest rate, the more money a customer need to pay the loan provider for a provided loan size.

The existing 2024-25 set rate of interest for Federal Direct Subsidized Loans and Direct Unsubsidized Loans for undergraduate trainees is 6.53%. The Federal PLUS loan (a federal moms and dad loan) has a set rate of 9.08%. The calculator also assumes that the loan will be paid back in equivalent monthly installations through basic loan amortization (i.e., standard or extended loan payment).

Top Questions Regarding Modern Debt Relief in 2026

Some academic loans have a minimum monthly payment. Please get in the appropriate figure ($50 for Direct Subsidized, Unsubsidized, and PLUS Loans) in the minimum payment field. Enter a greater figure to see how much cash you can save by paying off your debt quicker. It will likewise show you how long it will require to pay off the loan at the greater monthly payment.

The government pays the loan interest while a trainee remains in school. Unsubsidized loans are readily available to all students, no matter financial requirement. Students with unsubsidized loans are responsible for paying all interest on their loans. PLUS Loans are offered to biological, adoptive moms and dad, or stepparent of a reliant undergraduate student.

Loan fees, in some cases referred to as origination costs, are a small portion of the general loan expense. The lending institution establishes these charges, which serve as the processing charge to meet loans on the lender's side. Federal subsidized and unsubsidized student loans have an origination charge of 1.057%. Direct PLUS loans have an origination charge of 4.228%.

Comparing your student loan options is not simply a good concept, it's the very best way to conserve cash on the expense of loaning. Before you borrow, predict what your future payments might appear like by utilizing a loan payment calculator. This will offer you a clear image of your financial commitments.

How Certified Financial Advisory Works Today

Trustworthy deals customers a "kayak-style" experience while looking for personalized prequalified rates. Similar to the "Typical App," users (and co-signers) complete a single, brief form and get individualized prequalified rates from numerous loan providers. Inspecting rates on Credible is totally free and does not impact a user's credit rating to compare deals.

View Disclosures Customized Prequalified Rates on Credible is complimentary and does not affect your credit rating. Applying for or closing a loan will include a hard credit pull that affects your credit rating and closing a loan will result in expenses to you. Prequalified rates are based on the info you supply and a soft credit inquiry.

{kind=link}

Latest Posts

Benefits of Professional Financial Counseling Programs in 2026

Should You Consolidate Variable Credit for 2026?

Advantages of Certified Credit Programs in 2026